Table Of Content

Under "Down payment," enter the dollar amount of your down payment (if you’re buying) or the amount of equity you have (if refinancing). Or instead of entering a dollar amount, enter the down payment percentage in the window to the right. A down payment is the cash you pay upfront for a home, and home equity is the value of the home, minus what you owe. Interest rate - Estimate the interest rate on a new mortgage by checking Bankrate's mortgage rate tables for your area.

Rocket Mortgage

Your estimated annual property tax is based on the home purchase price. The total is divided by 12 months and applied to each monthly mortgage payment. If you know the specific amount of taxes, add as an annual total.

Mortgage Calculator: How Much Can I Borrow? - NerdWallet

Mortgage Calculator: How Much Can I Borrow?.

Posted: Mon, 26 Feb 2024 08:00:00 GMT [source]

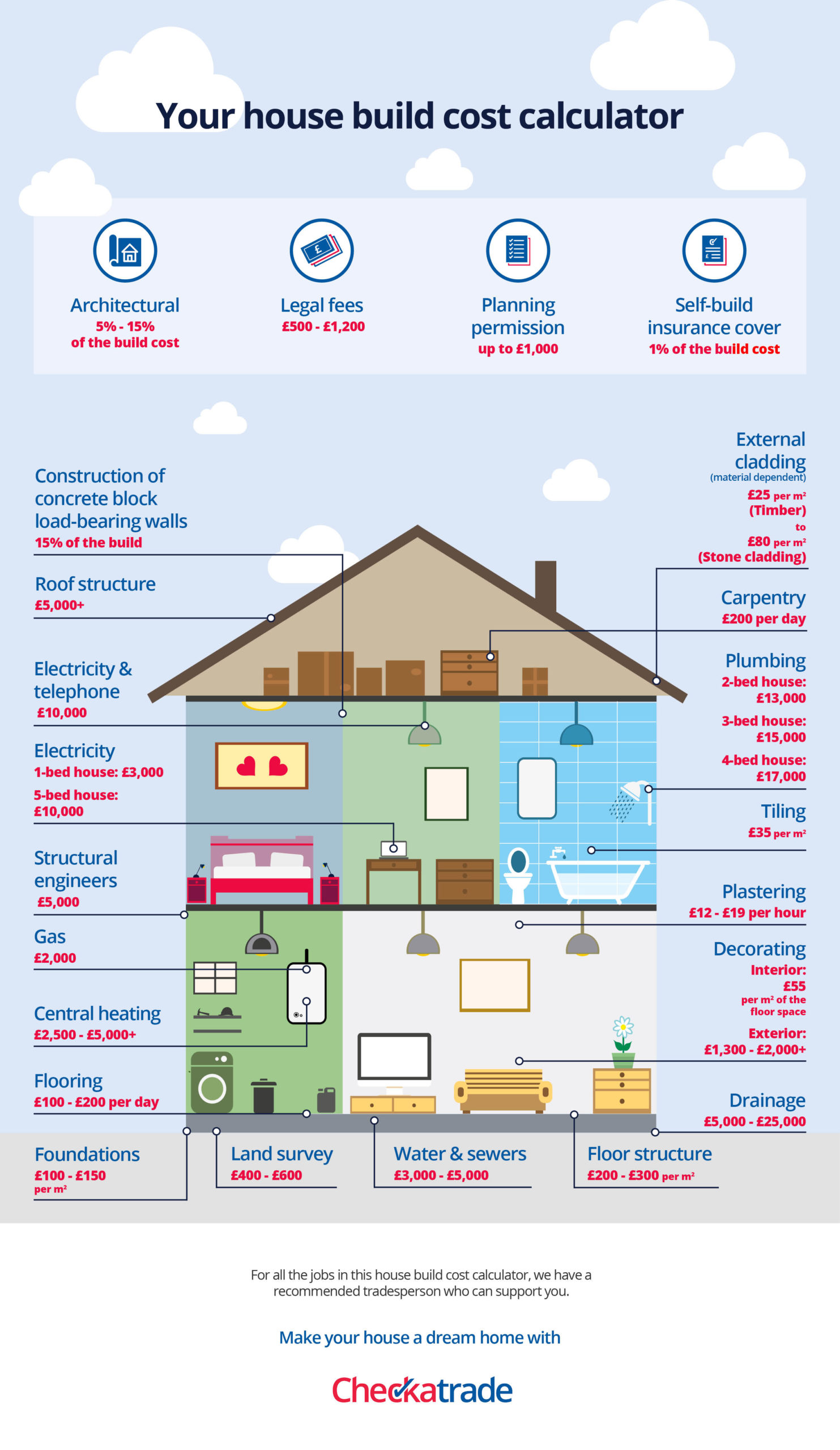

How much is homeowners insurance and what does it cover?

Typically, when you belong to a homeowners association, the dues are billed directly, and it's not added to the monthly mortgage payment. Because HOA dues can be easy to forget, they're included in NerdWallet's mortgage calculator. Your debt-to-income ratio is the percentage of pretax income that goes toward monthly debt payments, including the mortgage, car payments, student loans, minimum credit card payments and child support. Lenders look most favorably on debt-to-income ratios of 36% or less — or a maximum of $1,800 a month on an income of $5,000 a month before taxes. The mortgage calculator lets you click "Compare common loan types" to view a comparison of different loan terms. Click "Amortization" to see how the principal balance, principal paid (equity) and total interest paid change year by year.

Terms explained

Zillow's mortgage calculator gives you the opportunity to customize your mortgage details while making assumptions for fields you may not know quite yet. These autofill elements make the home loan calculator easy to use and can be updated at any point. You can think about refinancing (if you already have a loan) or shop around for other loan offers to make sure you’re getting the lowest interest rate possible.

How we make money

Adjustable-rate mortgage (ARM) loans are listed as an option in the [Loan Type] check boxes. Alternate loan durations can be selected and results can be filtered using the [Filter Results] button in the bottom left corner. You can select multiple durations at the same time to compare current rates and monthly payment amounts. Adding different information to the mortgage calculator will show you how your monthly payment changes.

If you want to explore an FHA loan further, use our FHA mortgage calculator for more details. Depending on your credit score, you may be qualified at a higher ratio, but generally, housing expenses shouldn’t exceed 28% of your monthly income. Mortgage lenders are required to assess your ability to repay the amount you want to borrow. A lot of factors go into that assessment, and the main one is debt-to-income ratio. Down payment - The down payment is money you give to the home's seller. At least 20 percent down typically lets you avoid mortgage insurance.

These loans have interest rates that reset at specific intervals. They typically begin with lower interest rates than fixed-rate loans, sometimes called teaser rates. After the initial term ends, the interest rate — and your monthly payment — increases or decreases annually based on an index, plus a margin.

That means determining the interest rate you will be charged. Your credit score largely determines the mortgage rate you’ll get. Get pre-qualified by a lender to see an even more accurate estimate of your monthly mortgage payment. There are several factors that determine your interest rate, including your loan type, loan amount, down payment amount and credit history. The term is the length of time you spend paying off the loan. The terms available to you will depend on your financial situation and the type of loan you choose.

A good affordability rule of thumb is to have three months of payments, including your housing payment and other monthly debts, in reserve. This will allow you to cover your mortgage payment in case of an unexpected event. If lenders determine you are mortgage-worthy, they will then price your loan.

This is the amount you borrow from your lender to buy your home. It’s factored into your monthly payment and paid off throughout the life of your loan. When lenders evaluate your ability to afford a home, they take into account only your present outstanding debts. They do not take into consideration if you want to set aside $250 every month for your retirement or if you’re expecting a baby and want to save additional funds. Loans backed by the FHA can also have more relaxed qualifying standards — something to consider if you have a lower credit score.

To remedy this situation, the government created the Federal Housing Administration (FHA) and Fannie Mae in the 1930s to bring liquidity, stability, and affordability to the mortgage market. Both entities helped to bring 30-year mortgages with more modest down payments and universal construction standards. Aside from paying off the mortgage loan entirely, typically, there are three main strategies that can be used to repay a mortgage loan earlier.

On desktop, under "Interest rate" (to the right), enter the rate. Under "Loan term," click the plus and minus signs to adjust the length of the mortgage in years. Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. Here is a list of our partners and here's how we make money.